Major Undertakings

Reading Hellworld #2

This is the second entry in the “Reading Hellworld” series, where I review and expand on various ideas addressed in the book and put them in conversation with ongoing events. In this entry, I return to the local government debt issues explored in Chapter 1 – “Buildings Devouring People” in light of the recent decision to launch a series of specialized bonds to fund key industries, arguing that this may constitute one of the most significant transformations of the financial system in China in decades. As usual, please note that the piece below has only been subject to light editing. I’ve also breezed through a few major periods of Chinese financial history, simplifying some of the dynamics at play in the turn-of-the-century reforms initiated by figures like Zhu Rongji. The book itself gets into some of these dynamics in more detail, as do the works cited below. But, if you notice any major errors, please shoot me a message!

Hellworld begins with the process of enclosure, detailing how the boom in built space across China has served, simultaneously, as the means through which the Chinese population has been made dependent on the market. In broad terms, the process in China mirrors that of postwar Japan and subsequent “late developers” more than that of “early developers” like the UK or US, where enclosure required the forcible “freeing” of the population from the land through state intervention on behalf of landowners. In the Chinese case, as elsewhere in East Asia, land reform ensured that many peasants were themselves property holders. Dispossession therefore occurred more through the pull factors of urbanization and spatial inequity than through the explicit pushing of the peasants off their land. The chapter’s title, “Buildings Devouring People,” highlights this contrast:

As sociologist Zhang Yulin argues, if Britain’s original enclosures could be characterized as ‘sheep devouring people’ for the way that they replaced peasants with livestock pasture (and thereby cast these former peasants into the fires of industry), then China’s enclosures might best be characterized as ‘buildings devouring people.’[1]

As the title suggests, the development of built space has itself served as a major driver of proletarianization.

But these physical transformations of territory are driven by social forces and facilitated through specific financial mechanisms tended by the state. For this reason, the bulk of the chapter is actually devoted to illustrating the process through which localities were starved of state revenue and thereby pitched against one another in “bidding wars” for investment and, most importantly, how this process then generated the unique forms of land financing that helped drive the developmental boom. Though initiated in the 1990s, land financing became even more important in the wake of the “great trade collapse” that followed from the 2008 crisis, allowing otherwise cash-strapped localities to compete for state infrastructural loans and industrial investment relocating from the coast. However, the unique role played by land in these financial schemes soon saw the emergence of a virtuous circuit: “Local governments … leveraged land to obtain loans, which financed the construction of everything from roads to business parks to the gargantuan megaprojects often associated with the Chinese developmental boom, all of which then further inflated the price of land.”[2]

As growth slowed, land prices and the real estate industry as a whole grew increasingly detached from industrial investment, resulting in the widely-reported real estate bubble, which was only the most obvious dimension of a general and multi-faceted growth in debt across any number of sectors. According to political economist Ho-fung Hung:

Between 2008 and late 2017, outstanding debt in China soared from 148 percent of GDP to over 250 percent. The 2020 pandemic brought a new surge of loans, which pushed the debt-GDP ratio to more than 330 percent, according to one estimate. Following well-worn grooves, most of this debt went to finance new apartments, coal plants, steel mills, and infrastructure projects. With few to consume their eventual output, the new investments merely generated further unprofitable excess capacity.

…

Falling profits add an urgent twist to the problem of indebted overcapacity. Profits provide firms with the cash flow to service their debts and pay back their loans. In China, the declining returns created a debt time-bomb: What would happen when the defaults started?

As a result, debt turnover became a key concern. New injections of credit were necessary just to roll over existing loans, leading to a series of bubbles accompanied by slowing growth in the private sector. As the economy entered into its “harsh winter,” narrow profits led to rapid consolidation of the strongest firms and bankruptcy for the rest, helping to drive waves of mechanization and offshoring, resulting in the gradual deindustrialization of employment – as explored in Chapters 3 and 5 of Hellworld.

Both the “private” and “public” sectors are ultimately manifestations of capital, or as different forms through which class power is expressed. It therefore makes little theoretical sense (unless you are a liberal) to treat “state” investment as representing some “non-capitalist” sphere of public interest or common good opposed to the narrow profit-seeking of the “capitalist” market.

This retrenchment of private investment then revealed the capital-intensive, low-profit bedrock of the economy which, in China as elsewhere, is structured by the state. Though portrayed as an “advance” of state-owned enterprises (SOEs), which then “crowded out” the private sector – a process widely codified in the media as “the state advances, the private sector retreats” (国进民退) – the real picture is more complicated. First, as much of Hellworld is devoted to demonstrating: both the “private” and “public” sectors are ultimately manifestations of capital, or as different forms through which class power is expressed. It therefore makes little theoretical sense (unless you are a liberal) to treat “state” investment as representing some “non-capitalist” sphere of public interest or common good opposed to the narrow profit-seeking of the “capitalist” market. Second, the simplistic narrative of state control over industry in China is also an empirical falsehood, misunderstanding:

the complex shareholding structures of all Chinese firms, within which essentially all major firms see a mix of “state” and “private” investment deriving from a wide variety of sources.

the more fundamental distinction between “inside the system” (体内) and “outside the system” (体外), which does not map onto “state” vs. “nonstate” or even “Party” vs. “non-Party.”

qualitative differences in economic institutions (i.e. an industrial SOE vs. a sovereign wealth fund vs. the Chinese Academy of Sciences vs. SASAC vs. a policy bank vs. the PBOC).

the comparative field itself – namely the fact that state investment is as large or larger as share of the economy in almost all wealthy countries, as compared to China (this is usually the most brazen example of Orientalism in such accounts).

the salient differences between levels of “state” investment (i.e. local government vs. municipal vs. provincial vs. central), usually accompanied by a tendency to treat all forms of state investment as somehow implying that a firm is controlled “by Beijing.”

What actually occurred in the 2010s was a slowing of private sector growth driven by the “great trade collapse,” accompanied by declines in profitability within private industry linked to mechanization, offshoring, and a general increase in average firm size (signaling that smaller firms either went bankrupt, grew into large conglomerates, or were absorbed into these conglomerates), all of which then left certain sectors bereft of private investment. Former World Bank head Justin Yifu Lin describes the basic dynamic at play: “the rising share and loan proportion of SOEs are consequences of the economic slowdown, not the cause. The reduced investment and loan shares of private enterprises result from external shocks and the overall economic slowdown.”[3] As a result, ongoing investments in infrastructure, public services, and cornerstone heavy industries (all of which, in China as elsewhere, have a more significant “state” component) came to compose a larger relative share of economic activity. The ongoing state-building project also saw state intervention grow more important to the functioning of the financial market in these years, both in injecting the liquidity necessary for the economy to survive its “harsh winter” and in defending against a catastrophic crash – as in the stock market crisis of 2015-16 or the crackdown on tech firm Alibaba (both an ecommerce giant and major fintech firm via its Ant Financial / Ant Group division) and real estate conglomerate Evergrande in 2020.

The following charts (all from Chapter 3) track these trends. The first demonstrates the increase in scale of Chinese enterprises, on average, as measured by output-per-enterprise:

The second shows the stagnation or decline in net profits after 2010 for all but the largest firms:

And the third shows trends in rate of return on assets among majority-private-invested and majority-state-invested firms, illustrating an initial divergence during the export boom, followed by a gradual convergence as private profits decline back toward the baseline of state-invested firms:

In part, these trends are linked to the lower average profitability of larger firms over time, paired with rapid declines in the profitability (and ensuing bankruptcies/mergers) of smaller firms, as can be seen when the series is disaggregated by size:

The formulation and refinement of the state’s industrial planning infrastructure has also helped direct investment (whether from specific state institutions or the capital market in general) toward the sectors that seem most capable of inducing the future growth necessary to pull the economy out of its “harsh winter” and into another spring in which these “green” industries (solar, nuclear, NEVs, biomanufacturing, and AI-enhanced agriculture) geared toward building an “ecological civilization” can finally bloom. This industrial aspect has not only been well documented in the media but has also become a salient factor in geopolitical contests, as cheap EVs produced by leading Chinese firms like BYD have flooded into the global market, utterly displacing their nearly-nonexistent competition and sending legacy automakers in the US scrambling back behind their tariff walls. While such accounts tend to overstate the cohesive, strategic nature of state industrial planning (and the structure of the state in general), they nonetheless grasp salient features of corporate strategy.

But the simultaneous process of fiscal and financial modernization is much less visible, though arguably far more important. The Tax Reform of 1994 discussed in Chapter 1, which deprived localities of tax revenue and thereby set the stage for the modern land-financing system, was among the most important early modernization measures. But that same year also saw the passage of the Company Law, which created a recognized legal status for limited liability and joint stock corporations. At the time, Zhu Rongji – the architect of China’s major financial reforms – was serving as vice-premiere and governor of the People’s Bank of China (PBOC), in which capacity he began to set the groundwork for the full-scale modernization of the entire financial system. A year earlier, at the National Finance Work Conference, Zhu stressed the need for a financial system that “must abide by the general laws of a market economy and gradually move us closer to international rules.” He also laid out his vision of what such a system would look like, modelled on the example set by countries like the US: “a system of financial institutions, under the supervision of the central bank, principally consisting of national policy banks and state-owned commercial banks, but that encompasses a variety of financial institutions.”[4]

More specifically, Zhu called for the formation of things like an interbank lending system, the creation of a market for short-term paper and a market-based RMB exchange rate system, an export-import bank, and a long-term bank specializing in developmental lending, all alongside the modernization of the stock market and corporate reforms to bring enterprise administration in line with global standards. Both an export-import bank and a development bank were then formed in 1994. But most of these suggestions only began to take shape after Zhu became premier in 1998. Chapters 5 and 6 discuss part of this process: the “corporatization” of Chinese industries, which saw the old SOEs split up and reconsolidated into modern corporations designed and funded, in part, by firms from Wall Street (which then gradually sold off their shares over the subsequent decades), which also helped them launch IPOs on the Hong Kong and New York stock exchanges. This period also saw the recapitalization of major banks and the sequestering of bad loans (on the model used in the Savings & Loan Crisis in the US) in the wake of the Asian Financial Crisis – all via the specially-designed investment firm Central Huijin, controlled by the central government and funded by foreign exchange reserves.[5]

In the early 2000s, PBOC governor Zhou Xiaochuan, working closely with Zhu, then pushed through a number of the initial reforms necessary to develop a bond market, which “would allow corporations to establish direct financial links with end investors and would also mean greater financial flexibility at times when stock markets were weak or unattractive.”[6] But these reforms soon slowed and, despite the fact that a large number of smaller financial institutions existed on paper, the sector remained relatively monopolized and corporate bonds did not become a major feature of the financial system. Corporate debt was an extremely low share of bond issuance in these years (a mere 3.5 percent in 2003) and, by the time of the Great Recession in 2008-09, finance was still centered almost entirely on the “Big 4” state-owned commercial banks (3 of which were corporatized by 2006), which drew mostly on record-high savings rates, as well as the PBOC’s purchase of US Treasuries and recycling of foreign exchange. In 2010, “these four banks controlled 45 percent of China’s total financial assets,” of which corporate bonds were a negligible share.[7]

These years also saw a number of innovations linking Chinese treasury bonds issued by the Ministry of Finance (MOF) to foreign exchange managed by the PBOC, which enabled the creation of sovereign wealth funds like the China Investment Corporation (CIC).[8] In the wake of the Great Recession, in addition to the Big 4 commercial banks – which dispersed many of the initial stimulus loans – sovereign funds like CIC and Central Huijin would grow increasingly important as mechanisms through which higher-level state policies could be pursued despite the persistent fragmentation of both state command chains (a major target of the Xi-era state-building campaign) and poorly-developed capital markets. As for the land-financing vehicles discussed in Chapter 1, the most significant feature of these years was the emergence of the shadow banking system to fill the financial gap left when reforms pursued by Zhu and Zhou slowed and the stimulus loans from commercial banks dried up. For context, in 2009, a total of roughly 4.7 trillion RMB of new loans were issued, mostly by the large commercial banks. Of these, “LGFVs obtained roughly 2.3 trillion, among which 2.06 trillion came from commercial banks and 0.26 trillion from policy banks.”[9]

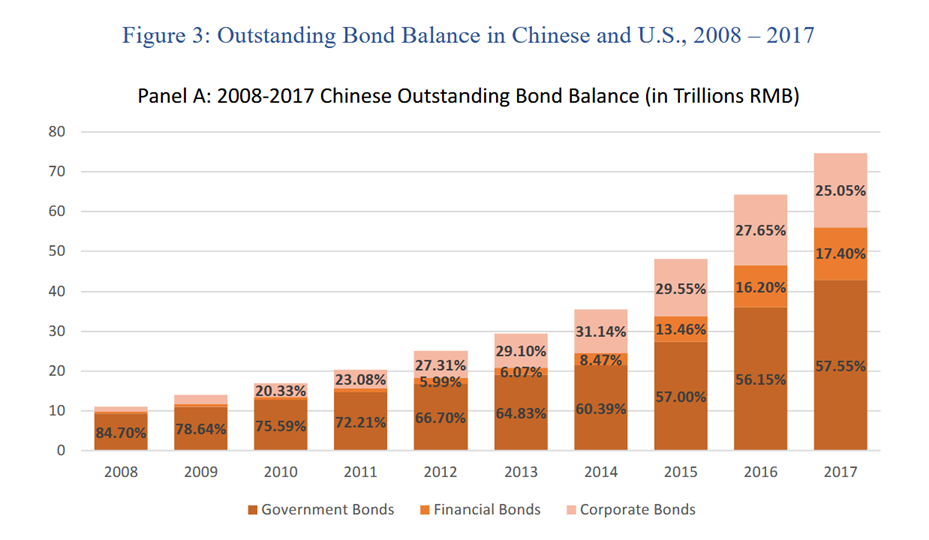

The category of “shadow banking” covers a wide range of financial markets unified mostly by their exclusion from the prevailing regulatory structure. In the Chinese case, major financial assets within the shadow banking system include “trust loans, WMPs [wealth management products], undiscounted bankers’ acceptances, [and] peer-to-peer lendings” among which trust loans and WMPs have been the most important.[10] However, given the stunting of the bond market, the 2010s also saw corporate bonds grow in importance and, because regulatory standards had never been established, these bonds operated as a form of shadow banking. Among these, municipal corporate bonds (MCBs, also called Chengtou/城投 bonds) issued by LGFVs were particularly important, as were Munibonds, which are the official form of municipal bond issued by local governments (though these can only be used to repay existing loans, in this case).[11] As a result, even while the absolute quantity of local government debt grew from just under 11 trillion RMB at the end of 2010 to just under 18 trillion RMB by mid-2013, bank loans as a share of total local government debt actually declined from 79% to 56.6% over the same time period, with the remainder made up of shadow banking assets like bonds, trusts, and “other.”[12] This mirrored trends in the economy as a whole, where bond balances grew as a share of GDP throughout the 2010s, including government bonds, financial bonds, and corporate bonds.[13]

As scholars like Yue Yuen Ang have noted (and as explored in Chapter 8 of Hellworld), the closest analog to the complex, public-private symbiosis that has driven the Chinese developmental boom is, in fact, the late-19th century US, where the productive corruption of the Gilded Age gradually gave way to the ramped-up state capacity and advancing regulatory regimes of the Populist and Progressive Eras. As Zhou et al. (2020) argue, the rise of LGFV-linked shadow banking in the 2010s in China effectively mirrors the shadow banking system that arose around trust companies in the National Banking Era in the US (roughly 1863 to 1913):

Whenever a fast-growing industry with a great business potential—railroads in the late 19th century in the US—is starved of funds, financial intermediaries figure out some ways to serve it. This is a recurring theme everywhere; our paper shows that China’s shadow banking activities can be viewed as regulatory arbitrages to serve the growing financing needs of LGFVs.

In the case of the US, the National Banking Act of 1864 imposed entry barriers and constraints on banking activities, which prevented the supply of banking services from keeping pace with the soaring demand as the country expanded westward. As a result, individual states started engaging in regulatory competition of banking legislations [sic].[14]

As in China, shadow banking also facilitated industrial investment and the expansion of credit and liquidity:

trust companies in the US invested in new industrial securities on the asset side of their balance sheets, while on the liability side, they expanded the money supply greatly, enabling the general public to gain access to new industries. The same economics underlie China’s shadow banking system today; AMPs [asset management plans…] hold corporate bonds (e.g., MCBs), financed by WMPs that become an important savings vehicle for Chinese households. This contributes to the expedited pace of interest rate liberalization in China after 2012.[15]

Finally, the US case also saw a link between infrastructure and a corporate bond market linked to land values via the intervention of local governments:

the unprecedentedly large-scale railroad finance during the late 19th century stimulated the development of a means for tapping public sources, leading segmented securities trading activities to evolve into the first major public market in corporate issues.

[…]

One of the leading examples is the corporate bond market […] the railroads constructed through the frontier West after 1850 primarily relied on public bonds […] In the 1850s, Henry V. Poor, the editor of American Railroad Journal, even advocated that municipalities guarantee the railroad bonds, just like MCBs in China.[16]

However, just as the US National Banking era was followed by a period of state-building and tightening regulation, resulting in the formation of the Federal Reserve and, thereby, the emergence of what would become modern macroeconomic management mechanisms, the 2020s have seen new rounds of fiscal and financial reforms geared toward displacing the shadow banking market and completing the modernization project initiated by Zhu in the 1990s. One aspect of this campaign has been the restructuring of local government debt and the increasing formalization of shadow banking activities, especially the corporate and municipal bond markets. But an even more important feature has been the refinement of the central government bond infrastructure toward the ideal of a modern macroeconomic system centered on the issuance of central-government-backed treasuries.

In late 2024, the shadow banking debt of LGFVs was rolled over via a debt swap aimed, in part, at exchanging “hidden” forms of debt for special bonds designed for the purpose. More stringent regulations were then rolled out to prevent local governments from engaging in new forms of shadow borrowing. For an overview of the process, see this translation of an article written by Minister of Finance Lan Fo’an:

The move was widely written off as yet another case of “extend and pretend” in which the debt load – which lay somewhere between 44 trillion and 58 trillion RMB by early 2025 – is simply rolled over into new asset classes without being reduced. But this appraisal largely ignores the overall context and fails to place the growth in the shadow banking system in historical context. During the National Banking era in the US, for example, the shadow banking system certainly included its fair share of speculation, as epitomized in the well-documented municipal streetcar and railway real estate scandals that plagued the era, known for its rampant corruption. But much of the demand for liquidity in this period was also linked to real infrastructural and industrial needs not adequately served by the official banking system. The subsequent populist and progressive reforms were therefore not simply aimed at reigning in corruption and speculation but also at constructing an adequate system of macroeconomic management centered on interlinked banking and bond markets anchored by the issuance of treasuries.

The LGFV restructuring of 2024 is therefore best understood when placed in the context of a growing and increasingly formalized bond market, including the expansion of long-term central government bonds. Though the transfer ostensibly only involves the deployment of “local government special-purpose bonds” to replenish LGFV funds, these special purpose bonds are more legible, more easily regulated, and also carry the stamp of the central state. In effect, this converts volatile forms of hidden debt backed only by local government guarantee into more well-recorded and, the hope is, more stable forms of debt at least loosely backed by the stronger guarantee of the central government. Although the step itself is small, the ultimate goal appears to be something similar to the slow transition from a shadow banking system subtended by local financial institutions to a more transparent and easily regulated banking system centered on the federal reserve in the early 20th century in the US – though, as always, these sort of historical analogies should be taken with a grain of salt.

The LGFV restructuring of 2024 is therefore best understood when placed in the context of a growing and increasingly formalized bond market, including the expansion of long-term central government bonds.

However, while the local government debt issue is the central fault line of the Chinese financial system and the growth of sovereign wealth funds has helped to enable an expansive industrial policy, the much less spectacular trends in Chinese treasury bonds are likely more important for etching out the long-term financial strategy articulated by Zhu. Particularly notable in this regard is the rising demand for Chinese government debt as a safe haven asset paired with the recent issuance of large sums in ultra-long bonds geared toward funding strategic sectors. In 2025, a government work report stated that “1.3 trillion yuan of ultra-long special treasury bonds will be issued, 300 billion more than last year” of which “735 billion yuan will be earmarked in the central government budget for investment.” Though long-term bonds are not new (including 30- and 50-year bonds), these “ultra-long special treasury bonds” have, until now, only been issued at a significant scale in response to three major events: the Asian Financial Crisis in 1998 (to recapitalize state banks), the establishment of CIC in 2007 mentioned above, and the pandemic in 2020 (used for fiscal support of relief measures). Similarly, while the issuance of Chinese treasury bonds has increased steadily over the years, the 2024-25 boost is 3 to 4 times the average volume of the preceding 3- and 5-year averages.

Reflecting declines in profit and the gradual deflation of the real estate bubble, many of the buyers have been domestic institutions and, across the economy as a whole, “ultra-long bond issuance has come to replace local government debt issuance, which fell by 14% in 2024.” By June of 2025, Chinese government debt comprised “about 27% of the balance sheets of large banks and up to 50% of smaller banks’ assets, according to surveys conducted by the PBOC – positions reflective of a broader derisking trend among institutional investors.”[17] In part, this is obviously a form of retrenchment, showing major institutional investors attempting to deleverage and retreat into safer asset classes in order to weather the storm and chip away at their debt load. And, in this regard, the behavior does seem to follow the “balance sheet recession” pattern identified by economist Richard Koo, who argues that the difference “between an ordinary recession and one that can produce a lost decade is that, in the latter, a large portion of the private sector is actually minimizing debt instead of maximizing profits following the bursting of a nation-wide asset price bubble.”[18] At the same time, however, the intervention is clearly intended to function as a backstop against precisely this sort of crisis, since “ultra-long bonds are an effective tool for debt restructuring, designed to shift the fiscal burden from overstretched local governments to the central government and its relatively strong balance sheet, greater debt capacity, and lower borrowing costs.”[19]

Much of this funding was then funneled into what have come to be known as the “two major undertakings” (两重). Originally laid out in the work report cited above as “the implementation of major national strategies and building up security capacity in key areas” (国家重大战略实施和重点领域安全能力建设), the “two undertakings” has since turned into a key phrase, often linked to the building up of the so-called “new productive forces” or “new quality productive forces” (新质生产力) referenced in central government texts since 2023 and applied to a wide range of decarbonization technologies like solar panels, batteries, and NEVs as well as “frontier” scientific endeavors in fields ranging from aeronautics to biomanufacturing. Given their long-run, often infrastructural nature, however, conventional funding methods are not ideal for national security projects, public services, or long-range R&D in new sectors. This is another major reason for the current approach: “ultra-long bonds lock in capital for many years, they are ideal for funding long-term strategic projects such as China’s new productive forces.”[20] Meanwhile, the ultra-long treasuries will be accompanied by a similar boom in newly-approved corporate bonds earmarked for similar projects.

According to Cong Yu, the Executive Vice President of Tsinghua University’s Institute for China Development Planning and former official at the National Development and Reform Commission (NDRC):

Compared with previous special bond issuances, the funding for the two undertakings spans a longer cycle and serves a wider range of purposes, with plans for continued implementation.

[…]

In terms of priorities, it vividly reflects the principle of “concentrating resources to accomplish major undertakings.” The focus areas include urban–rural integration, regional coordination, high-quality population development, food security, energy and resource security, ecological security, and self-reliance and strength in science and technology

And, perhaps most importantly, this represents a new level and entirely different style of central government influence over investment:

The organization of the “two major undertakings” construction is top-down, completely different from the past practice in the investment sector where projects were determined through bottom-up applications. The purpose is to facilitate the smoother downward transmission of the needs of major national strategies. Relevant [central] government departments, by identifying shortcomings and weaknesses, specifying key areas, and refining project requirements, have ensured that the project list is no longer a collection of fragmented local items. Instead, projects are planned in an integrated manner by category and sector, with strengthened guidance for key regions, more targeted measures, and clearer standards.

A full translation of Dong’s article is available over on Pekingology:

Though still somewhat vague, with no exhaustive list of projects yet available, many of the exact priorities will no doubt be laid out in full in the upcoming 15th Five-Year Plan. But, on the surface, the shift seems to be in keeping with the general trend and, rather than a divergence from liberalization, is fully consistent with both the outline set by Zhu in the 1990s and with the arc of development observed in places like the US, where the National Banking era gave way to the Federal Reserve, which then enabled both the more thorough-going macroeconomic interventions piloted in the 1920s (which were crucial factors in the defeat of rising labor militancy, as explained by Adam Tooze) and expansive national-strategic projects like the New Deal of the 1930s or the wartime mobilization of the 1940s, which seemed, in their own moment, to be a classic case of the “state advances, the private sector retreats” (国进民退) but were, in retrospect, always the singular advance of capital in its two guises.

[1] Hellworld, p.44

[2] ibid p.43

[3] Qtd. in ibid, p.184

[4] Qtd. in Zongyuan Zoe Liu, Sovereign Funds: How the Communist Party of China Finances Its Global Ambitions, The Belknap Press of Harvard University Press, 2023. p.47

[5] This paragraph can only barely due justice to the complex series of reforms that occurred in these years. In addition to Liu 2023, a particularly good overview of the financial reforms in this period can be found in: Carl E. Walter and Fraser J.T. Howie, Red Capitalism: The Fragile Financial Foundation of China’s Extraordinary Rise, Singapore: John Wiley & Sons Singapore, 2011,

[6] Walter and Howie 2011, p.15

[7] ibid, p.29

[8] See Liu 2023, Chapter 3

[9] Zhuo Chen, He Zhiguo, and Liu Chun, “The financing of local government in China: Stimulus loan wanes and shadow banking waxes”, Journal of Financial Economics, 137, 2020. p.47

[10] ibid, p.48

[11] For an overview of the logic behind MCBs, see: Thomas Walker, Zhang Xueying, Zhang Aoran, and Wang Yulin, “Fact or fiction: Implicit government guarantees in China’s corporate bond market”, Journal of International Money and Finance, 116 (102414), September 2021.

[12] ibid, Table 1, p.47

[13] Marlene Amstad and He Zhiguo, “Chinese Bond Market and Interbank Market”, NBER Working Paper 22549, February 2019. Figure 3, p.48

[14] Zhuo et. al. 2020, p.66

[15] ibid

[16] ibid, p.67

[17] Christopher Vassalo and Wallace Mathai-Davis, “Will Ultra-Long Bonds Help Beijing Capitalize Its ‘New Productive Forces’?” Asia Society Policy Institute, 03 June 2025. <https://asiasociety.org/policy-institute/will-ultra-long-bonds-help-beijing-capitalize-its-new-productive-forces#footnoteref8_Lboh6G48pihpOLOvmWtEUMWjchOYIaO2up37xJ5YYY_g8oHFhlCU47h>

[18] Koo grew to prominence through his widely-circulated paper on the Great Recession, which drew on his earlier research and experience within the Japanese real estate crash. His books on the subject are worth checking out, particularly The Holy Grail of Macroeconomics: Lessons from Japan’s Great Recession (New York: Wiley, 2009).

[19] Vassalo and Mathai-Davis 2025.

[20] ibid